ACA Plans and Generic Coverage: What You Actually Get Under the Affordable Care Act

Nov, 20 2025

Nov, 20 2025

When you hear ACA plans, you might think of cheap health insurance. But what you actually get? That’s where things get real. The Affordable Care Act didn’t just make insurance more affordable-it changed what insurance even means. Before 2010, if you had diabetes, cancer, or even asthma, insurers could deny you coverage or charge you triple. Now? They can’t. That’s not a perk. That’s a lifeline.

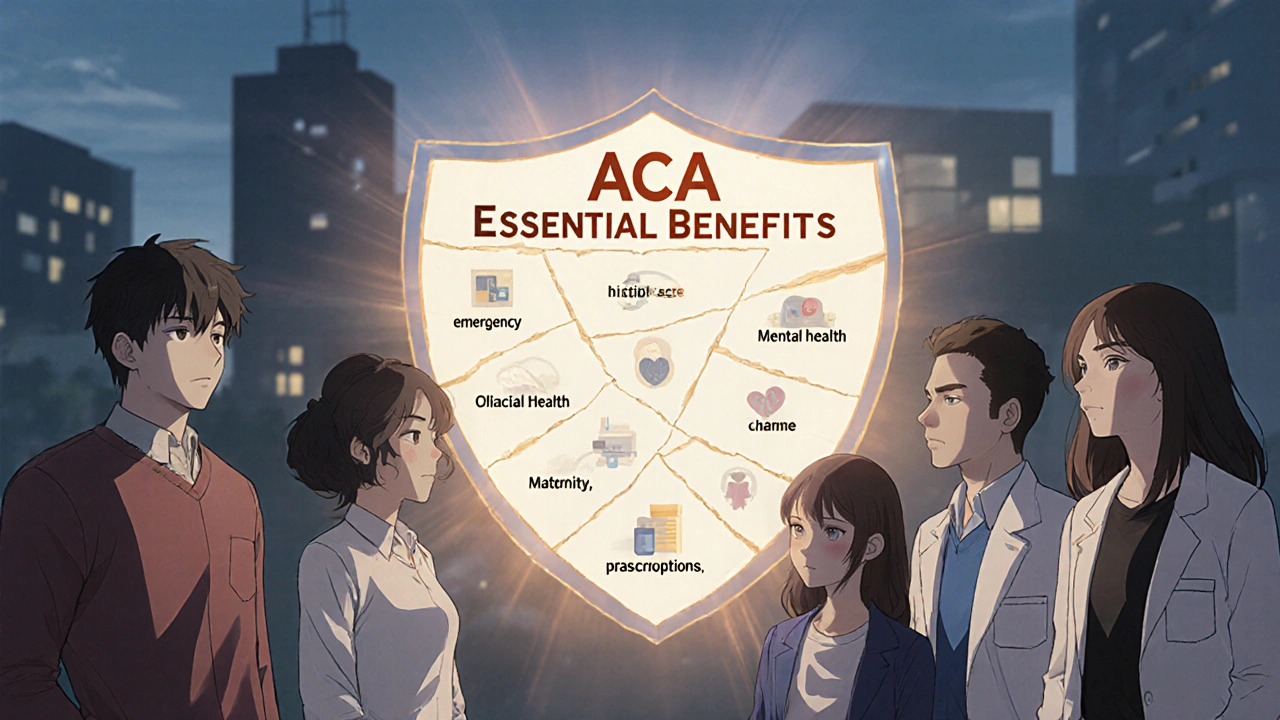

What’s Included in Every ACA Plan

Every ACA Marketplace plan-whether it’s Bronze, Silver, Gold, or Platinum-must cover ten essential health benefits. No exceptions. No fine print loopholes. These aren’t optional add-ons. They’re the baseline. That means:

- Ambulatory patient services (outpatient doctor visits)

- Emergency care

- Hospitalization

- Pregnancy, maternity, and newborn care

- Mental health and substance use disorder services

- Prescription drugs

- Rehabilitative and habilitative services

- Laboratory services

- Preventive and wellness services

- Pediatric services, including dental and vision

If your plan doesn’t cover one of these, it’s not an ACA plan. Period. And that’s the point. Before the ACA, insurers sold plans that looked cheap but skipped everything important-like maternity care or mental health. People ended up with bills they couldn’t pay because their plan didn’t cover what they needed. The ACA fixed that.

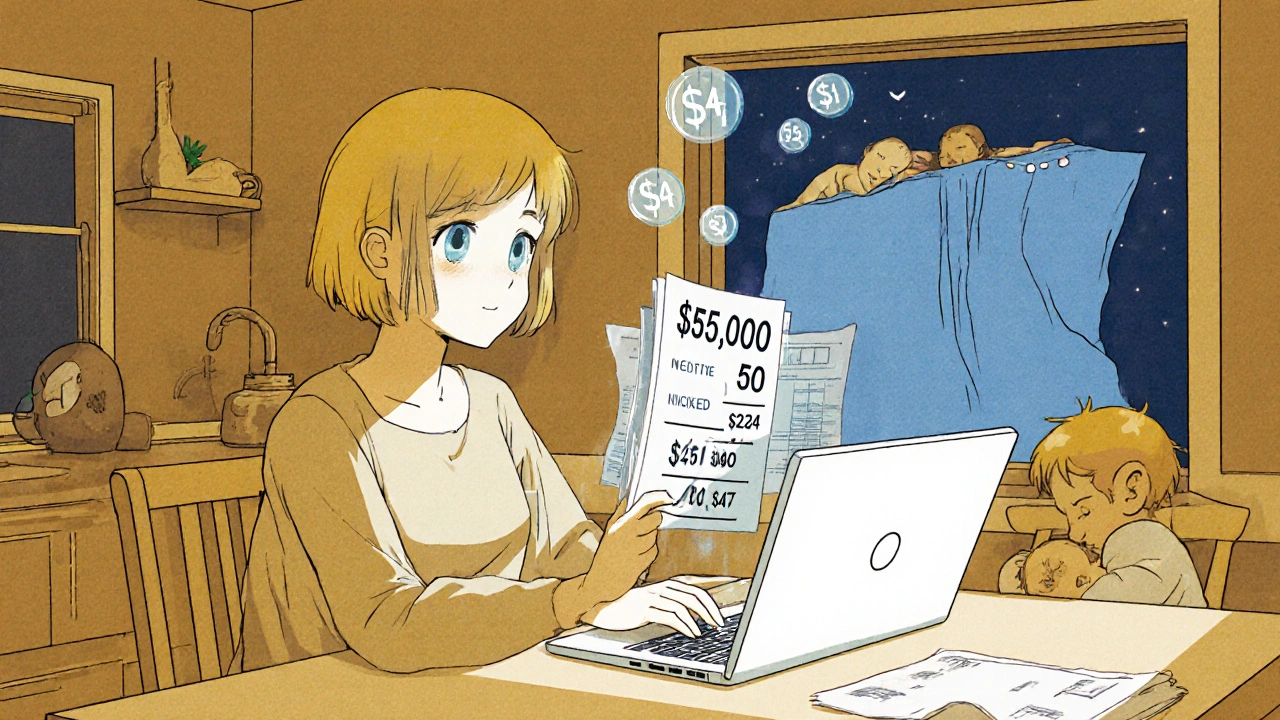

How Premium Tax Credits Actually Work

Most people don’t pay full price for their ACA plan. They get help. That help is called a premium tax credit. It’s not a discount you apply at checkout. It’s money sent directly to your insurer to lower your monthly bill.

Right now, if your household income is between 100% and 400% of the Federal Poverty Level (FPL), you qualify. For a single person in 2025, that’s $15,060 to $60,240 a year. If you make $50,000, you could pay as little as $247 a month for a Silver plan-with enhanced credits. Without them? $534. That’s not a small difference. That’s $3,456 a year you don’t have to spend.

But here’s the catch: those enhanced credits expire at the end of 2025. If Congress doesn’t act, your premium could jump by over 100% next year. For a 60-year-old in some states, it could be nearly double. That’s not a policy tweak. That’s a financial earthquake for millions.

Metal Tiers: Bronze, Silver, Gold, Platinum

Don’t be fooled by the names. Bronze isn’t cheap because it’s bad-it’s cheap because you pay more when you use care. Silver is the sweet spot for most people, especially if you qualify for cost-sharing reductions (CSRs). Those are extra discounts on deductibles and copays that only apply to Silver plans.

Here’s the breakdown:

| Plan Tier | Actuarial Value | What You Pay | Best For |

|---|---|---|---|

| Bronze | 60% | 40% of costs | Healthy people who rarely see doctors |

| Silver | 70% | 30% of costs | Most people-especially if you get CSRs |

| Gold | 80% | 20% of costs | People who use care regularly |

| Platinum | 90% | 10% of costs | Chronic conditions, frequent hospital visits |

Most people who get subsidies pick Silver. Why? Because if your income is below 250% FPL, you get extra help lowering your out-of-pocket costs-like lower deductibles and copays. That’s called a cost-sharing reduction. It’s not automatic. You have to pick a Silver plan to get it.

Who Gets Left Out?

Not everyone qualifies. DACA recipients were eligible until November 2025. Now, they’re not. That’s about 550,000 people losing coverage. It’s not a loophole-it’s a policy change. And it’s not just about paperwork. It’s about people who’ve been paying taxes, working, and raising families suddenly losing access to care.

Also, if you’re over 400% FPL and don’t get insurance from your job, you get no subsidy. That’s the “subsidy cliff.” Make $1 more than $60,240 as a single person? Your premium jumps from $300 to $800 a month overnight. No warning. No grace period. That’s why so many people are stuck between jobs or working gig work-they’re terrified of crossing that line.

The Enrollment Trap

Applying for an ACA plan sounds simple. It’s not. You need your Social Security number, pay stubs, tax returns, and proof of citizenship or immigration status. If you’re self-employed? You need bank statements, profit/loss statements, and sometimes even invoices. The system asks for your Modified Adjusted Gross Income (MAGI). Most people don’t know what that is.

And here’s the kicker: your subsidy is based on what you estimate your income will be. If you’re wrong? You pay the difference at tax time. One Reddit user, u/ACA_Warrior, got hit with $2,800 in unexpected bills because his income dropped mid-year and he couldn’t adjust his subsidy until next April. That’s not a glitch. That’s how the system works.

The new 2025 CMS rule tries to fix this by requiring quarterly income updates starting in 2026. That’s good. But it’s also a burden. If you’re a freelancer with fluctuating income, you’ll need to log in every three months and update your numbers. Miss one? Your subsidy could disappear.

Why ACA Plans Are Still the Best Option for Millions

Yes, the system is messy. Yes, the rules change. Yes, you can get hit with a tax bill if your income shifts. But here’s what no one else offers: guaranteed coverage for pre-existing conditions. No lifetime caps. No annual limits. Coverage for mental health and addiction treatment that actually matches physical health benefits.

Compare that to short-term plans-those “cheap” alternatives that exclude everything. Or employer plans that leave your family out because of the “family glitch” (which was fixed in 2023, but most people still don’t know about it). Or Medicaid, which is better-but only if you’re under 138% FPL.

For a freelance writer in Ohio making $32,000 a year? She gets a $0 premium Silver plan with full cost-sharing reductions. That’s not luck. That’s policy. That’s the ACA working exactly as designed.

What’s Coming in 2026

If the enhanced tax credits expire, the Marketplace will shrink. The Kaiser Family Foundation predicts a 15-20% drop in enrollment. Premiums could jump 25-35% in the first year. Older adults, low-income families, and people in non-expansion states will be hit hardest.

And the new rules? They’re tightening verification. You’ll need to prove your income more often. Your eligibility might be checked against IRS data more aggressively. That’s meant to stop fraud. But it also means more people will get dropped-accidentally-because of a mismatched W-2 or a late tax filing.

What’s clear? The ACA isn’t perfect. But it’s the only system that gives real protection to people who need it most. The alternatives? They’re not better. They’re just cheaper on paper. Until you get sick.

What You Should Do Now

If you’re enrolled in an ACA plan:

- Check your income estimate. If you’ve had a change-job loss, raise, new baby-update it now. Don’t wait until tax season.

- Make sure you’re on a Silver plan if you qualify for cost-sharing reductions. That’s where the real savings are.

- Know your out-of-pocket maximum. For 2025, it’s $9,450 for an individual. No plan can charge you more than that in a year.

- Start saving for 2026. If subsidies expire, your bill could double. Set aside $100 a month now to cover the gap.

- Don’t cancel your plan just because you think you can find something cheaper. Short-term plans and health sharing ministries aren’t insurance. They won’t cover your cancer treatment.

The ACA isn’t about politics. It’s about whether you can get care when you need it. Right now, 17.3 million Americans rely on it. For most, it’s the only thing standing between them and financial ruin.

Leah Beazy

November 22, 2025 AT 07:02Just got my renewal notice and my premium dropped to $0. Seriously. Silver plan, full CSR, and I didn't even have to fight for it. The ACA saved my life when I got diagnosed with lupus. No one talks about that part.

Before this, I was choosing between insulin and rent. Now? I just pay my copay and go.

Stop acting like this is some socialist fantasy. It's basic human decency.

And yes, I'm terrified about 2026. But I'm not giving up.

Anyone else in the same boat?

Let's start a thread for people who need this stuff.

It's not charity. It's survival.

John Villamayor

November 22, 2025 AT 16:28Look I get it but why do we keep pretending this system is perfect

My cousin got denied a CT scan because it wasnt 'medically necessary' under his Gold plan

Turns out he had a tumor

He had to wait 3 months and pay out of pocket

Thats not coverage thats a gamble

And dont get me started on the paperwork

My grandma cried filling out her application

She's 72 and still works part time

She shouldn't have to be a tax lawyer to get health care

Jenna Hobbs

November 24, 2025 AT 13:40YALL. I just wanna say this: I used to hate the ACA. Thought it was government overreach. Then my daughter got diagnosed with Type 1 diabetes at age 5.

Before ACA? We would’ve been bankrupt by month 3.

Now? We pay $18 a month for her insulin. The rest? Covered.

I used to think health care was a privilege. Now I know it’s a right.

And if you’re saying we should go back to the old way? You’ve never held your kid while she cries because her blood sugar is 480.

Thank you, ACA. I’ll fight for you every day.

❤️

Ophelia Q

November 25, 2025 AT 00:05Just want to say thank you to the person who wrote this. I’m a single mom working two jobs. My Silver plan with CSR lets me see my therapist once a week. Without it? I’d be lost.

Also, the 2026 cliff? I’ve been saving $75 a month since January. Not glamorous, but it’s what I can do.

And yes, I know my MAGI. I keep a spreadsheet. 😅

You’re not alone. We’re all in this together.

Elliott Jackson

November 25, 2025 AT 21:35Let’s be real - this whole thing is a circus. You think you’re getting care? Nah. You’re getting a membership to the insurance bureaucracy.

My brother got approved for a MRI… after 6 months. Then they said the facility wasn’t in-network. So he paid $4,200 out of pocket.

And now they want us to update our income every 90 days? Like we’re some kind of freelance algorithm?

It’s not healthcare. It’s a customer service nightmare with a side of existential dread.

And don’t even get me started on the ‘essential benefits’ that don’t include chiropractic or acupuncture.

Why is mental health covered but not my back pain?

That’s not equity. That’s politics with a stethoscope.

McKayla Carda

November 25, 2025 AT 23:03My mom got on Medicaid last year. She’s 68, works part-time, makes $12k. No subsidy. No ACA. Just Medicaid.

She’s fine now. But if she made $1 more? She’d lose everything.

That’s the cliff. And it’s real.

Don’t let anyone tell you otherwise.

Christopher Ramsbottom-Isherwood

November 26, 2025 AT 20:19Interesting how you call this a lifeline but ignore the fact that millions are priced out because of the subsidy cliff

Also why is Silver the 'sweet spot'? Because the government wants you to pick it so they can give you extra subsidies

That’s not freedom. That’s manipulation

And if you’re not on a Silver plan you’re basically being punished for not being poor enough

Also who decided that pediatric dental is essential but adult orthodontics isn’t?

That’s not medicine. That’s social engineering

Stacy Reed

November 27, 2025 AT 04:14But what if the ACA is just a band-aid on a bullet wound?

What if the real problem is that healthcare in America is a for-profit industry?

And we’re all just arguing over which brand of band-aid to use?

Why don’t we talk about single-payer?

Why do we accept this? Why do we celebrate a system that still leaves people bankrupt?

Isn’t it strange that we call this 'progress' when someone still has to choose between insulin and rent?

Maybe the real issue isn’t the ACA… it’s that we’ve normalized suffering as a cost of doing business.

Is that really the world we want?

Robert Gallagher

November 27, 2025 AT 07:13I’m a freelance photographer. Income goes up and down like a rollercoaster.

Last year I made $58k. Got the full subsidy. This year I made $62k. Lost it all.

My premium went from $220 to $890.

And I didn’t even get a warning.

They just said 'you’re over the limit.'

So I switched to a Bronze plan.

Now I pay $1,200 every time I go to the ER.

Guess what? I haven’t been to a doctor in 11 months.

That’s not insurance. That’s fear.

And yeah, I’m saving $100 a month for 2026.

But I’m not holding my breath.

Howard Lee

November 28, 2025 AT 03:46Correction: The family glitch was fixed in 2023, but the fix only applies to plans offered through employers with 50+ employees. Many small businesses still exclude dependents. So the glitch persists for millions. Also, the out-of-pocket maximum for 2025 is $9,450 for individuals and $18,900 for families. Not $9,450 for families. Important distinction.

Nicole Carpentier

November 28, 2025 AT 21:35My brother works at a gas station. Makes $14/hr. No benefits.

He’s on a Silver plan with CSR. Pays $18/month.

His kid has asthma. They go to the ER maybe twice a year.

He says the plan saved his life.

He doesn’t know what MAGI is.

He doesn’t care.

He just knows he can breathe.

That’s all that matters.

Hadrian D'Souza

November 30, 2025 AT 13:50Oh look, another love letter to the bureaucratic monster that turns healthcare into a spreadsheet game.

You call this 'lifeline'? It’s a rigged casino where the house always wins.

People don’t die because they lack insurance.

They die because the system is designed to make them wait.

And you? You’re just here to pat yourself on the back for not being the one who got dropped.

Meanwhile, the real villains? The CEOs who make $20M while you fight over $300 in tax credits.

But sure. Keep optimizing your Silver plan. It’s very brave.

Brandon Benzi

December 2, 2025 AT 07:05ACA is a socialist trap. Why should hardworking Americans pay for people who don’t want to work?

My dad served in Vietnam. He never got free healthcare. He paid for his own. He didn’t cry about it.

Now we have people getting $0 premiums while I pay $800 a month for my job-based plan.

It’s not fair.

And DACA recipients? They’re not citizens. Why are they getting this?

This isn’t healthcare. It’s welfare with a stethoscope.

Abhay Chitnis

December 2, 2025 AT 08:45Bro I'm from India and we have universal healthcare

But I came to the US and saw this ACA mess

It's like a broken ATM that sometimes gives you cash

Other times it swallows your card and says 'try again next year'

Why does America make simple things so complicated?

Even my grandma in Delhi understands health insurance better than most Americans

And she doesn't even have a smartphone

Robert Spiece

December 3, 2025 AT 03:21Let’s not pretend this is about care.

This is about control.

Who gets to decide what’s 'essential'?

Who gets to say your mental health is covered but your chronic pain isn’t?

Who gets to say your subsidy disappears if you earn $1 over the line?

It’s not a system. It’s a power play.

And the people who benefit? They’re not the ones getting care.

They’re the ones getting political capital.

And you? You’re just the collateral.

Wake up.

Vivian Quinones

December 4, 2025 AT 10:21Why do we keep pretending this is about health?

It’s about control. Who gets to live. Who gets to die.

They don’t want you healthy.

They want you grateful.

They want you to thank them for the $0 premium.

But what if you don’t want a handout?

What if you want justice?

What if you want to be treated like a human?

Not a number.

Not a MAGI.

Just a person.

That’s what we’re really fighting for.

Eric Pelletier

December 5, 2025 AT 01:29For those confused about MAGI - it’s Modified Adjusted Gross Income. It’s your AGI from your tax return, plus tax-exempt interest, foreign earned income, and certain other exclusions. The Marketplace uses it to calculate subsidy eligibility. If you’re self-employed, you’ll need to project your annual income based on year-to-date earnings, plus any expected changes. If you’re wrong, you’ll reconcile on Form 8962. Pro tip: Use the IRS’s Subsidy Estimator tool. It’s not perfect, but it’s better than guessing.

Marshall Pope

December 6, 2025 AT 13:08yo i just wanna say i got my plan last year and it saved me

my back went out and i had to go to the er

they charged me $150

that was it

i didnt have to sell my car or ask my mom for money

so thanks aca

even if the website is a mess

and i still dont know what magi means

but i know i can breathe

and thats enough

Leah Beazy

December 7, 2025 AT 12:52Just saw your comment, Marshall. I’m crying. That’s exactly why I fight for this.

It’s not about the system. It’s about people.

And you? You’re one of them.

Don’t let anyone tell you your story doesn’t matter.

You’re not a number.

You’re not a MAGI.

You’re human.

And you deserve care.

Thank you for saying that.